Winning with money is not an easy path to walk. The experience can definitely feel like a walk through the mud. If financial success had a mascot, it would definitely be the iconic tortoise from “The Tortoise and the Hare.” How does the Tortoise win with a clear disadvantage and the odds stacked against him? I bet if we had a chance to ask him, we would find that he’s got a lot of grit.

In her popular Ted Talk, University of Pennsylvania Professor and Psychologist Angela Lee Duckworth defines “grit” as “passion and perseverance for very long-term goals.” She continues to explain that “grit is stamina, and sticking with your future – not just for the day, not just for the month, but for years.”

Check out her full talk here.

Duckworth’s research has even shown that “grittier” kids are significantly more likely to graduate!

If it is true that grit determines success more than IQ, what makes up grit? Is there a way to harness the power of grit to achieve financial independence? How would you define “financial grit?”

Here’s my suggestion:

Goal-driven…

Responses to daily situations that…

Incrementally increase our likelihood to win over…

Time

Every piece of this gritty puzzle is just as important as the next. Without all elements, our ability to build and harness true financial grit falters, and we may fall short of our goals.

Let’s take a look at what makes up our financial toughness. It’s time to channel our inner-amphibians and officially declare the tortoise as our financial spirit animal.

Goal-Driven

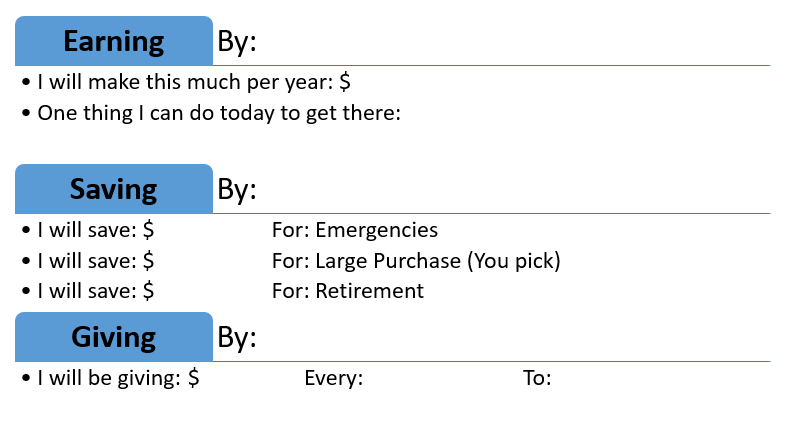

This is the why behind what we do. Without clearly defined and relevant goals, we will jump ship at the slightest sign of rough waters. Using the Focus Finder is a great way to transform our greatest aspirations into daily goals, but let’s take a minute to focus on financial goal-setting. Here’s a framework for financial goal-setting that will get your gears turning. On a sheet of paper, word doc, or spreadsheet, build the following template:

Now get going on filling it out! This template will clearly lay out for you your financial goals in three key areas: earning, saving, and giving. Make sure to pay attention to the fact that we should save for three things – emergencies, large purchases (cars, homes, college, vacations), and retirement.

Once you have your baseline goals on paper, break your goal amounts into monthly amounts, and decide how your income and budget can support your vision. If something’s off – adjust!

Responses to Daily Situations

Have you ever heard the phrase “death by a thousand cuts?”

This is a good visual of how we usually end up in financial distress. It’s not like we wake up one morning and just decide that we are going to live a miserable life buried by tons of consumer debt. No, typically these things take time, with a healthy dose of denial or just flat-out ignorance. We’ve all been there, but how do we get out of this mess?

The answer is simple – the same way we got in – by making thousands of tiny decisions.

To stand at the starting line of a marathon is a daunting and terrifying thing, but once we realize that the only thing we have immediate control over is our next step – it becomes manageable. 26.2 miles? Scary. 1 step? Easy!

This is how perseverance and passion can be maintained, and why setting manageable, daily, behavior-based financial benchmarks can be so incredibly empowering. Here are some examples of what daily financial benchmarks might look like:

- Make it to 5 pm without spending money.

- Track my purchases at the end of every day, or every morning with my coffee.

- Have one non-confrontational, 3-minute conversation with someone I love about money each day.

- Wear a bracelet with a mantra on it to remind myself of my long-term goals every time I think about signing into Amazon.

- Listen to 1 motivational financial speaker a day.

- Read 1 chapter of a personal finance book a day.

- Pack my lunch.

- Use a crock-pot so that dinner is ready when I get home and don’t feel like cooking.

What would you add to the list?

Incrementally Increasing My Likelihood to Win

Once we set up a system to make better daily decisions, the cumulative results of our better behavior will begin adding up. This is the fun part, but let’s go in with both eyes wide open. To see the fruits of our labor, we’re going to have to stick with our plan – for a long time.

Remember, grit is a marathon, not a sprint. The odds of winning a 6-digit lotto are 1 in 200 million. That’s not a race i’m willing to bet on. This instant-gratification seeking behavior is exactly what lost the hare his race. I’d much rather set a slower pace, with methodical performance checks, proper fueling, and a TON of support to get me to the big prize.

Here’s where we look up from our daily behavior goals and set monthly or bi-annual benchmarks. All that’s required is 6th grade math. Here’s an example:

Daily goal: Pack my lunch.

Savings: $15

Work-days a month I would have eaten out for lunch: 15

Monthly checkpoint: $15 x 15 days = $225

Yahtzee! Now make it a 6-month goal.

$225 x 6 = $1,350

What could you do with another $1,350 every 6 months? That’s what I call incremental progress. This is just one example. Incremental progress can (and should) be tracked over longer periods of time, especially when it comes to saving for retirement.

Over Time

So here’s the kicker. We are really good at what we focus on. The end-game is to develop enough grit to maintain focus for a really, really, really long time. In the “Tortoise and the Hare,” the tortoise’s ability to focus for the duration of the race lead to him besting an un-focused and arrogant opponent.

We need to follow the tortoise’s example when it comes to the ability to sustain focus for a long time. How long do you ask? That all depends on how you filled out the goal matrix above. For a car it may be a few years. For big ticket items like college and a home – longer still. For retirement, you will most likely have to display a lifetime of grit. It will be hard, but definitely worth it. Here’s an example of how perseverance and passion can pay off over time:

Say that our goal is retirement, and we want to live off of 4% of our nest-egg each year for as long as possible. This is a commonly used number, and our hope is that our investments will return an average of 4% or more per year, so that we preserve as much principal as possible to pass onto our family! If you feel that’s too high, you can run your own projections for what you’d like to use.

So if we’re going with the 4% rule, then we need to figure out:

A. How much money do we need annually to live in retirement?

B. What is that number 4% of?

***With this being a discussion on the benefits of saving, we won’t factor in inflation here, but just know that you will need a little more money each year from your investments and passive income to afford the same quality of life. Things will simply cost more because of inflation.***

Let’s say that after careful analysis of our expenses, we determine that we need $50,000 a year to live comfortably if we were to retire tomorrow. The answer to question A is $50,000.

Then we take $50,000 and divide by .04 to determine what 50k is 4% of…the answer being $1,250,000. There’s our retirement savings goal!

Using a standard time value of money calculator like the one found at investor.gov, we can find that in order to save $1,250,000 over 40 years, we’d have to invest $521.79 a month. Assumptions here are 7% rate of return – just be sure to run at different return rates and time-horizons to see how these variables will affect your outcomes.

That’s one way to do it. The other way is to simply plug in how much you’re budget allows you to save, and see what you might end up with. Say our budget only allows us to invest $100/month. In 40 years at 7% return, you would still end up with $241,059.58. Not a million, but WAY better than if you hadn’t saved at all!

Disclaimer: This is just an example of one scenario with a steady rate of return, which isn’t very common in equity markets. To get the most specific and realistic plan for your situation, you should meet with a fiduciary financial planner.

The benefit of time in investing cannot be overstated. If you have an income and time, whether it be 40 years or 5, there is no better time to start investing than right now. Your future self will be glad you did.

Get Some Grit

The more that your daily responses to hundreds of decisions are in line with your purpose and goals, the greater your chance of winning over time. Use these tools and formulas to start transforming your aspirations into manageable daily tasks. Remember, Rome wasn’t built in a day, and true grit won’t be build overnight. You can do this – it’s time to take that first step in your personal race, then another, then another. It’s time to get gritty.